The Week Ahead: Bank Earnings, Oil Prices, and Stock Market Recovery in Focus

TLDR

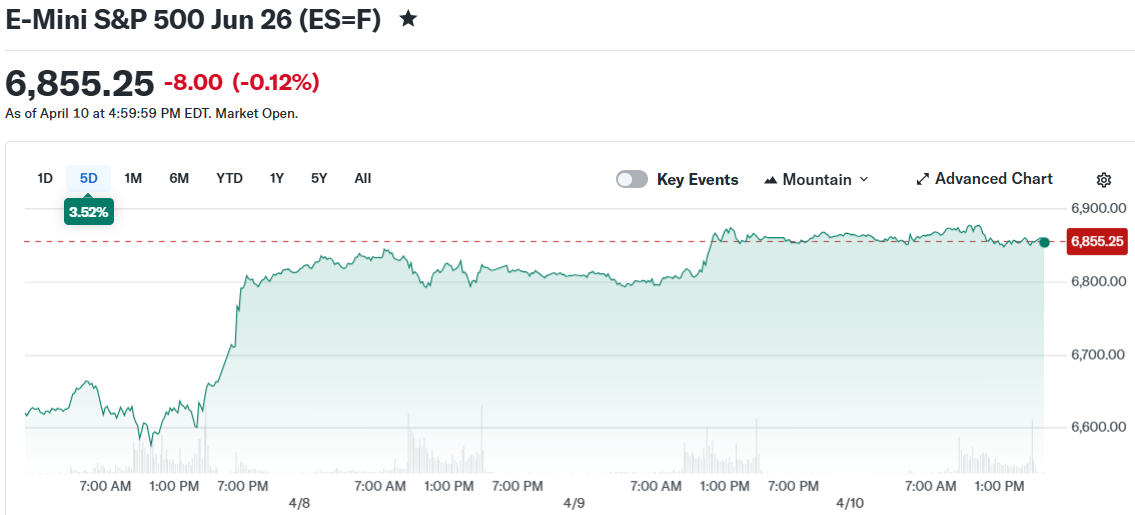

- Stocks posted a second straight winning week, with the S&P 500 up 3.5%, Dow up 3%, and Nasdaq up 4.7%

- Big bank earnings from JPMorgan, Goldman Sachs, Bank of America, and others report this week

- March CPI showed the largest monthly inflation increase since June 2022, driven by energy prices

- Oil sits near $98 a barrel but futures suggest a drop toward $85 by July, which could lift stocks

- Software stocks are deep in the red for 2026, while semiconductor stocks are up over 20% year to date

Stocks wrapped up their second consecutive winning week as investors turned their attention to the start of earnings season. The S&P 500 gained 3.5%, the Dow rose 3%, and the Nasdaq climbed 4.7% for the week. All three indexes are still down for the year but are now within 1% of breaking even.

E-Mini S&P 500 Jun 26 (ES=F)

E-Mini S&P 500 Jun 26 (ES=F)

The week ahead brings a heavy earnings schedule. Goldman Sachs reports Monday. JPMorgan Chase, Citigroup, and Wells Fargo follow on Tuesday. Bank of America and Morgan Stanley report Wednesday, with Netflix and Taiwan Semiconductor due Thursday.

Markets are also watching geopolitical developments closely. US-Iran talks in Pakistan over the weekend failed to produce a peace deal after Tehran refused to agree not to develop a nuclear weapon, according to Vice President JD Vance late Saturday.

Oil Is the Key Number to Watch

Since the US-Iran war began, oil has been the single most watched data point in markets. West Texas Intermediate crude closed Friday near $98 a barrel, up sharply from around $68 before the conflict started.

However, futures for July delivery are pricing oil closer to $85. Julian Emanuel of Evercore ISI said WTI in the “low-to-mid $80s” would be enough to remove the headwind on stocks.

The two-week ceasefire between the US, Israel, and Iran gave markets a boost last week. Whether that holds will shape the direction of oil and, by extension, the broader market.

Friday’s CPI report showed headline prices rose 0.9% in March, the largest monthly gain since June 2022. Economists noted most of that increase was tied to the energy spike from the conflict.

Consumer sentiment from the University of Michigan hit a record low in April, though 98% of those responses were collected before the ceasefire was announced.

Source: Forex Factory

Source: Forex Factory

Software Stocks Fall While Chip Stocks Rise

The split inside the stock market has widened. The iShares Software Sector ETF fell more than 7% last week and is now down 30% for the year.

Salesforce is the biggest drag, down over 35% in 2026. AppLovin, Intuit, and ServiceNow are each off more than 40%. Microsoft, Palantir, and Oracle are each down more than 25%.

Semiconductor stocks tell a different story. The VanEck Semiconductor ETF is up over 20% this year. Intel, Applied Materials, Lam Research, and Marvell Technologies are each up more than 50%.

ASML reports Wednesday, and Taiwan Semiconductor reports Thursday. Taiwan Semiconductor pre-reported strong March revenues last week, pointing to continued AI chip demand.

Netflix is also set to report Thursday, rounding out a packed week for earnings.

The post The Week Ahead: Bank Earnings, Oil Prices, and Stock Market Recovery in Focus appeared first on CoinCentral.

You May Also Like

SUI Price Prediction as Pepeto Tops $8.8M Before Listing

Morning Crypto Report — XRP Scores Best ETF Week Since February With $11.75 Million, Bitcoin Fails $74,000 Breakout Ahead of Tuesday’s April 14 PPI Data, Shiba Inu (SHIB) Coils for 33% Move as Volatility Hits Rare Lows