Bitcoin Price Drops 14% After Record High – Is It Just a Healthy Correction?

- Bitcoin slid 14% from $124,474 to $107,350 after U.S. inflation data shook investor sentiment.

- Traders still expect a Fed rate cut in September, with odds rising to 87.6% despite the recent pullback.

- On-chain signals show long-term accumulation, stable miner reserves, and no signs of market euphoria.

Bitcoin is down nearly 14% since breaking its record high of $124,474 on Aug. 14 to a weekend low of $107,350. The decline has shaken the traders and set off a huge amount of discussion in the marketplace. The correction came after the issue of the July U.S. Personal Consumption Expenditures (PCE) price index. The data suggested more inflation than predicted, deflating investor confidence.

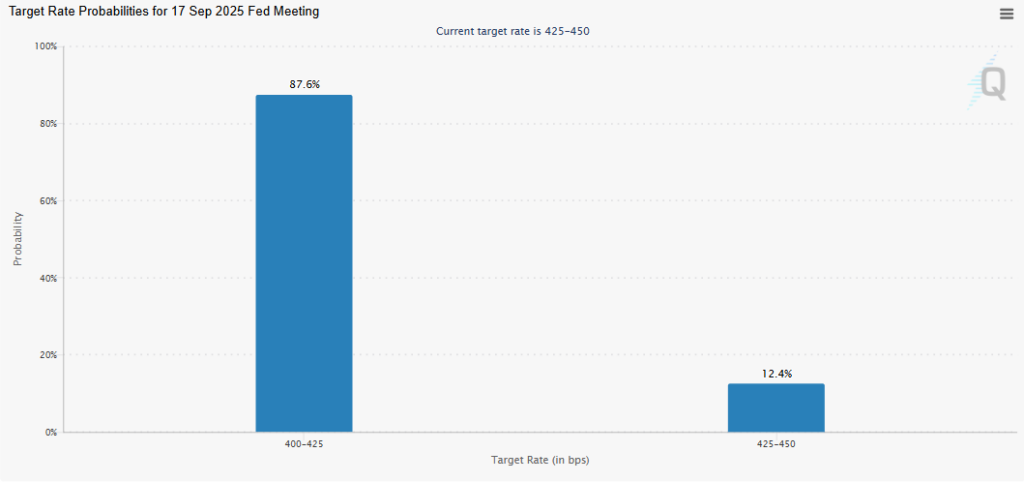

Despite the correction, traders are optimistic about a monetary easing from the Federal Reserve. According to the CME FedWatch tool, which tracks the odds of a rate cut or hike, the odds of a 25 basis point reduction in September are now 87.6% as opposed to an 85% pre-PCE data release figure.

Source: CME Group

Source: CME Group

Bitcoin Pullback: Weak September or Hidden Strength?

August was not a great month for Bitcoin, which finished down 6.49%. According to CoinGlass, the historically weakest September for the cryptocurrency is an average of a 3.5% decrease.

Source: Coinglass

Source: Coinglass

Also Read: Bitcoin Targets $92K and $117K CME Gaps Amid Liquidity Surge

The recent pullback has rekindled the conversation about the long-term trajectory of Bitcoin. Some market observers worry that the cryptocurrency is on the verge of hitting a cycle peak—others counter that this is merely a healthy contraction within a still ongoing bull cycle. On-chain data supports the latter view, with long-term holder accumulation and falling reserves on exchanges indicating relatively weak selling pressure.

Historically, in each Bitcoin bull market there have been sharp corrections that ultimately led to new highs. CryptoQuant analysts cite compelling fundamentals that remain intact, such as growing institutional adoption, rising interest in spot ETFs, and growing opportunity in the areas of tokenization and decentralized finance (DeFi).

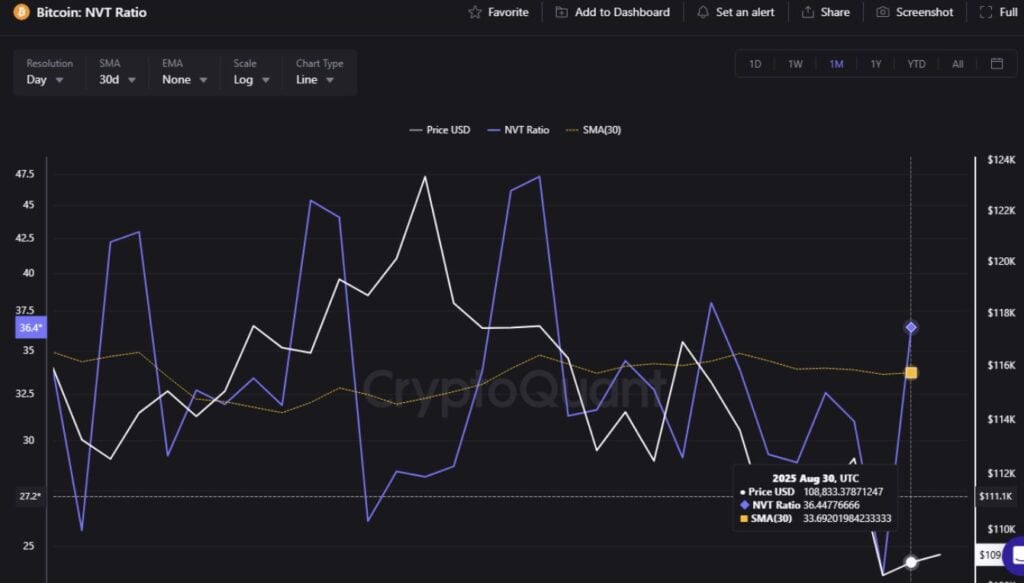

There are several important indicators that Bitcoin is not, in fact, running hot just yet. Market capitalization relative to transaction volumes (also known as the NVT ratio) has been below 50 since July 7. In these circumstances Bitcoin may be undervalued relative to network activity, something typical for longer term growth.

Source: X

Source: X

NVT and MVRV Ratios Signal Stability

Another important factor to look at is the MVRV ratio. Historical tank top readings near 3.6 have coincided with cycle tops and all-time highs. At this point, the signal is still far below that level, which means that they have no idea of market euphoria. Analysts take this as an indication that the cryptocurrency is not yet in the exuberant phase mentioned above, as seen during previous peaks.

Miner activity can also be used as a gauge of long-term optimism. The current holdings of miners amount to 1.805 million BTC and have barely changed this year, dropping by only about 6,000 BTC. While miners may sell heavily towards the tops of previous market totes to lock in gains, such pressure has not materialized and suggests an expectation that further price appreciation is on the cards in the coming period.

Source: X

Source: X

Similarly, aSOPR (whether or not coins moved on-chain are sold at profit) tends towards the mid-range. Over 1 usually indicates overvaluation and general euphoria among market participants, but readings are stable right now. This implies that whilst most coins continue to be profitable, profit-taking is not at levels that typically signal the end of a cycle.

All these pillars together paint a picture of resilience. While the short term may be volatile, the fundamentals are strong, and the longer-term metrics continue to build the business case for continued expansion. If in September the Fed lowers interest rates and institutional demand increases, Bitcoin could break out of its summer weakness and pave the way for another rise.

Also Read: Bitcoin Bears Eye $105,000 Support as Metaplanet Expands Holdings

คุณอาจชอบเช่นกัน

Financing Weekly Report | 13 public financing events; Privacy blockchain Miden completes $25 million seed round, led by a16z Crypto and others

Tesla Sees $657M Outflows As South Korean Retail Investors Favor Crypto-Related Stocks