CoinShares: BTC loses favor, assets under management reach new all-time high on 12th week of inflows

Price gains over the past week boost total assets under management up to a new all-time high of $188 billion. CoinShares noted a shift in investor attitudes which favored Ethereum more than Bitcoin.

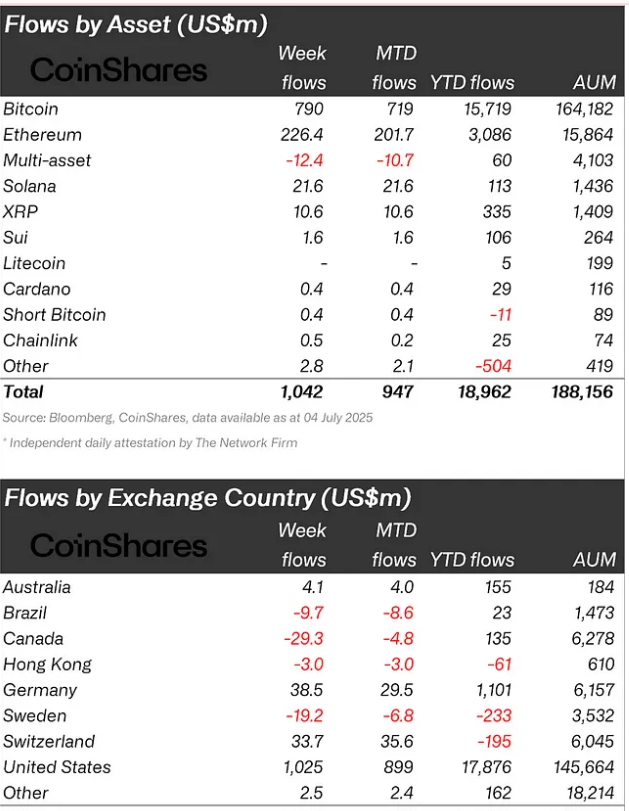

In the past week, digital asset investment products saw $1.04 billion in global inflows, which marked the 12th consecutive week of inflows. According to CoinShares’ weekly report, the total net inflows have reached $16.3 billion, which aligns with the weekly average of 2025 so far.

Not only that, price gains evident throughout the last week also pushed the AuM to a new all-time high of $188 billion from its previous $187.5 billion record. Although Bitcoin (BTC) still contributed the largest share of inflows, with $790 million last week, it marked a significant decline from the previous three weeks.

Bitcoin held up an average of $1.5 billion in inflows within the past three weeks. However now it has dipped by nearly 50% this week alone. According to Head of CoinShares research, James Butterfill, noted that the slowdown in Bitcoin’s performance indicates that investors are growing cautious of betting their funds on the largest cryptocurrency by marketcap.

“The moderation in inflows suggests that investors are becoming more cautious as Bitcoin approaches its all-time high price levels,” said Butterfill.

In fact, he noted that there has been a shift in investors’ attitude towards Ethereum (ETH), which recorded its 11th week of consecutive inflows with $226 million. According to the CoinShares report, weekly inflows from ETH throughout last week’s period amounted to 1.6% of the total assets under management.

Butterfill observed that this rate was significantly higher than the 0.8% contributed by Bitcoin, which he believes is a sign that more investors are warming up towards Ethereum while keeping a safe distance from Bitcoin.

From a regional standpoint, the United States still holds the largest share of inflows last week with $1 billion in inflows. Meanwhile, Germany and Switzerland also saw inflows with $38.5 million and $33.7 million respectively. On the other hand, Canada and Sweden experienced outflows amounting to $29.3 million and $19.2 million.

Other regions such as Hong Kong and Brazil saw modest outflows of $3 million and $9.7 million.

You May Also Like

Circle issues another $250 million USDC on Solana

UK Treasury Targets Crypto Tax Evaders with £300 Fines Starting January 2026