Lending

Share

Lending protocols form the backbone of the decentralized money market, allowing users to lend or borrow digital assets without intermediaries. Using smart contracts, platforms like Aave and Morpho automate interest rates based on supply and demand while requiring over-collateralization for security. The 2026 lending landscape features advanced permissionless vaults and institutional-grade credit lines. This tag covers the evolution of capital efficiency, liquidations, and the integration of diverse collateral types, including LSTs and tokenized RWAs.

14404 Articles

Created: 2026/02/02 18:52

Updated: 2026/02/02 18:52

Can the popular RWA really make money?

Author: PANews

2025/09/10

Share

Recommended by active authors

Latest Articles

Which Is The Best Crypto To Buy In This Bear Market? Remittix Tops Global Charts After Viral 300% Offer

2026/02/07 03:25

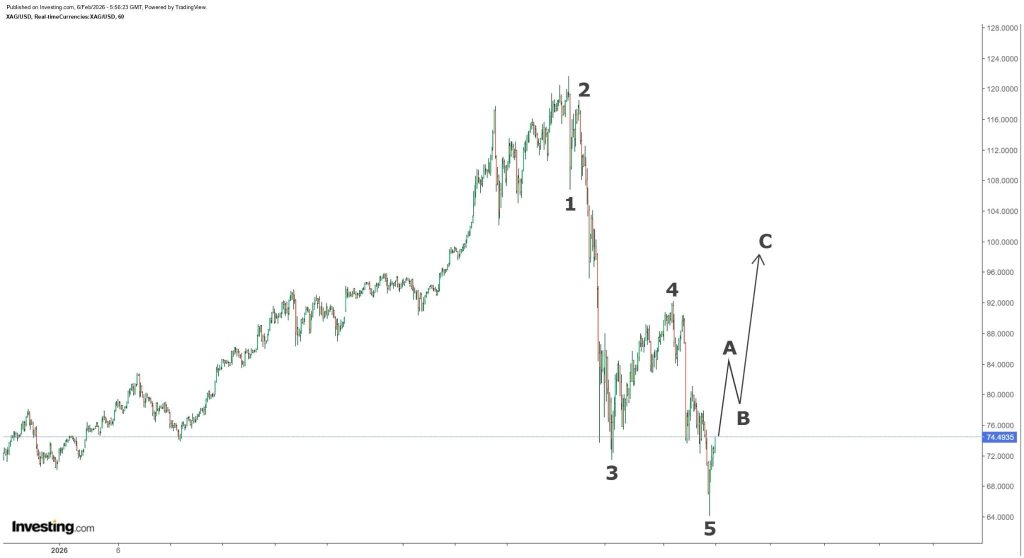

Silver Price Crash Is Over “For Real This Time,” Analyst Predicts a Surge Back Above $90

2026/02/07 03:15

The Daily: Strategy’s ok unless BTC falls to $8K, Charles Hoskinson’s down over $3B in crypto, Bithumb mistakenly sends bitcoin to users, and more

2026/02/07 03:03

Ripple CEO Hints at Buying Opportunity Amid Crashing Crypto Prices

2026/02/07 02:58

Strategy, BitMine, Coinbase Shares Chart Major Rebound as Bitcoin Stabilizes

2026/02/07 02:49